- Have any Questions ?

- info@capstoneplanet.com

How Long Does Underwriting Take? The Real 2026 Timeline Breakdown

This guide breaks down exactly what’s happening behind the scenes during underwriting why your file might be taking longer than your neighbor’s and the specific steps you can take right now to avoid the most common delays .

Key Takeaways

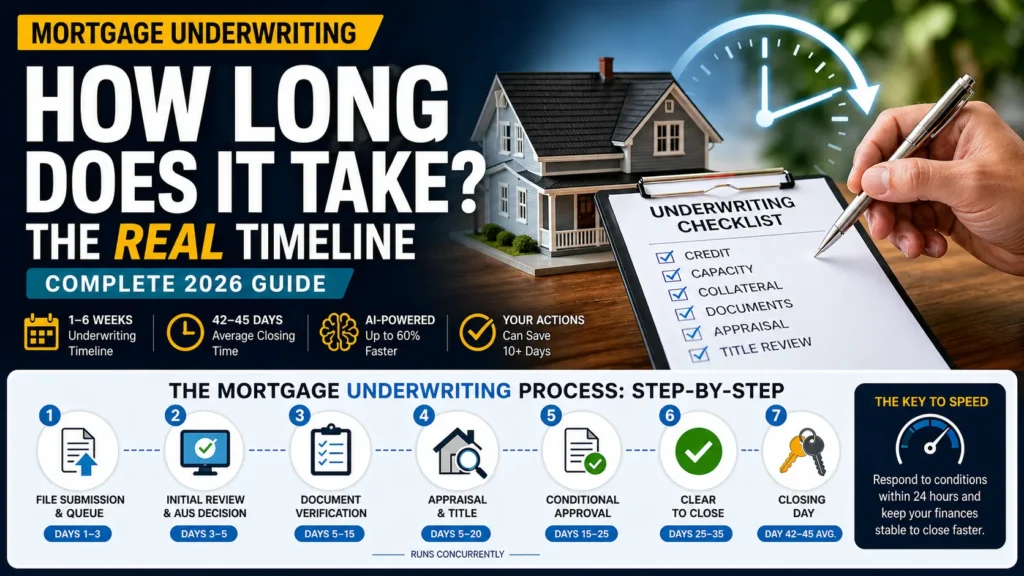

- Average Timeline : Mortgage underwriting takes 1–6 weeks total closing averages 42–45 days .

- Biggest Delay Cause : Missing or incomplete documentation accounts for the majority of underwriting holdups .

- AUS Speed : Automated Underwriting Systems can return a preliminary decision in minutes but full approval still requires human verification .

- 2026 Shift : AI-augmented underwriting is cutting processing times by up to 60% at tech forward lenders .

- Your Control: Borrowers who respond to conditions within 24 hours close an average of 10 days faster .

What Exactly Happens During Underwriting?

Before we talk timelines you need to understand what an underwriter actually does with your file . An underwriter isn’t just ” approving ” your loan they’re conducting a deep forensic analysis of your financial life to answer one question Is this person a safe bet ?

The industry breaks this down into the ” Three C’s “ of underwriting:

- Credit : Your credit history score and repayment behavior they’re looking at your FICO score outstanding debts late payments collections and credit utilization ratio .

- Capacity : Can you actually afford this ? They verify your income employment stability and debt-to-income (DTI) ratio to ensure monthly payments won’t stretch you too thin .

- Collateral: Is the property worth the loan amount ? this is where the home appraisal comes in if the house appraises below the purchase price your loan could hit a wall .

Every piece of paper you submitted pay stubs W-2s tax returns bank statements gets cross referenced verified and scrutinized . It’s thorough by design your lender is putting hundreds of thousands of dollars on the line and the underwriter is the last line of defense .

The Step-by-Step Underwriting Timeline

Here’s how the process unfolds from the moment your application enters the underwriting queue :

Step 1: File Submission and Queue (Days 1–3)

Your loan processor compiles your complete file and submits it to the underwriting department . Depending on the lender’s current volume your file may sit in a queue for 1–3 business days before an underwriter even opens it . During peak seasons ( spring and summer buying ) this wait can stretch longer .

Step 2 : Initial Review and AUS Decision (Days 3–5)

The underwriter runs your file through an Automated Underwriting System (AUS) typically Fannie Mae’s Desktop Underwriter (DU) or Freddie Mac’s Loan Product Advisor (LPA) . This system returns one of three results :

- Approve/Eligible : Your file meets automated guidelines great news this speeds things up significantly .

- Refer/Eligible : Your file needs a closer human look not a denial but it adds time .

- Refer with Caution : Red flags exist expect a deep manual review .

Step 3 : Document Verification (Days 5–15)

This is where the clock really starts ticking or stalling the underwriter verifies every claim in your application :

- Employment verification (calling your employer or using automated services)

- Income documentation cross referencing (pay stubs vs tax returns vs bank deposits)

- Asset verification (checking that your down payment funds are ” seasoned ” and sourced properly)

- Reviewing your debt obligations and calculating your final DTI ratio

If everything checks out cleanly you’re in good shape but any discrepancya large unexplained deposit a gap in employment an inconsistency between documents triggers additional questions and extends the timeline.

Step 4 : Appraisal and Title (Concurrent Days 5–20)

While the underwriter reviews your financials, two critical third party processes run simultaneously :

- Home Appraisal : A licensed appraiser visits the property to determine its fair market value this typically takes 1–2 weeks to schedule and complete. If the appraisal comes in low, you’ll need to renegotiate the purchase price or bring additional funds to close.

- Title Search: A title company investigates the property’s legal history to ensure there are no liens unpaid taxes ownership disputes or easement issues that could block the sale .

Step 5 : Conditional Approval (Days 15–25)

Here’s something most borrowers don’t expect getting ” conditionally approved ” is the norm not the exception. About 80–90% of all mortgage applications receive a conditional approval rather than a clean outright approval. This means the underwriter is saying : “You’re approved, but I need a few more things first.”

Common conditions include:

- An updated pay stub or bank statement

- A letter of explanation (LOE) for a large deposit or credit inquiry

- Proof of homeowner’s insurance

- A signed gift letter if your down payment includes family funds

Your response speed here is everything borrowers who return conditions within 24 hours can shave a full week off the process. Those who drag their feet for 5–7 days They’re the ones complaining that underwriting took forever.

Step 6 : Clear to Close (Days 25–35)

Once all conditions are satisfied the underwriter issues the golden ticket : ” Clear to Close ” (CTC). At least three business days before closing you’ll receive a Closing Disclosure (CD) outlining your final loan terms interest rate monthly payment and total closing costs. This mandatory 3-day waiting period is required by federal law ( TRID rule ) so you can review the numbers without pressure.

Step 7 : Closing Day

You sign the final documents wire your down payment and closing costs and the property is legally yours . The entire journey from application to closing averages 42–45 days with underwriting consuming the largest and most variable chunk of that timeline .

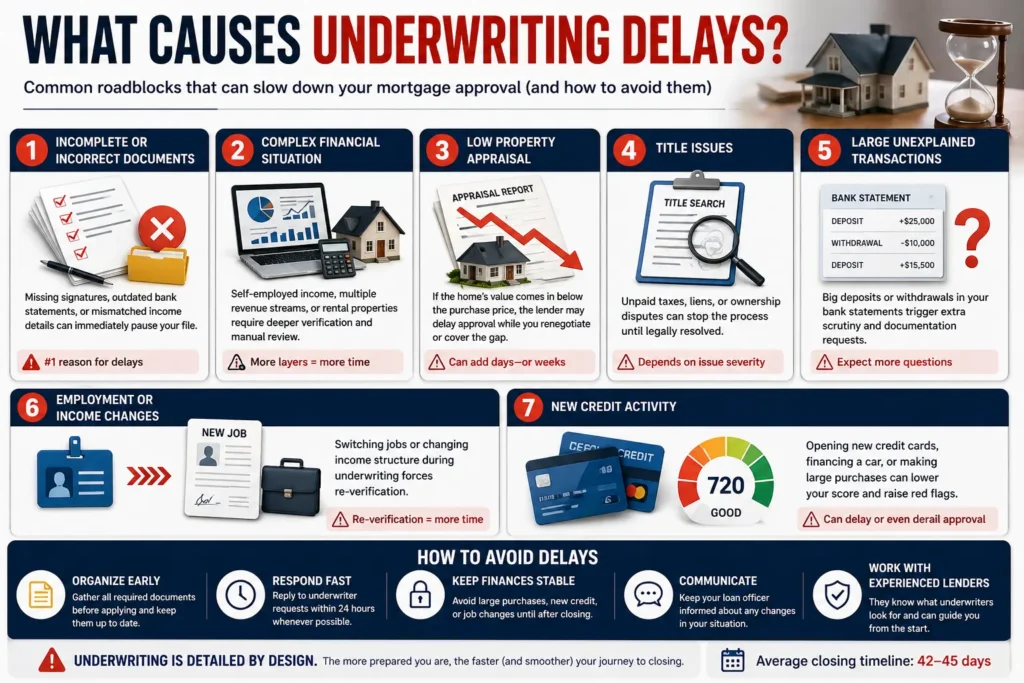

What Causes Underwriting Delays? (And How to Avoid Them)

You can’t control everything but you can control the biggest delay triggers here are the top reasons files get stuck and exactly what to do about each one :

1. Incomplete or Inaccurate Documentation

This is the number one cause of underwriting delays period missing signatures outdated bank statements or tax returns that don’t match your W2 income will trigger a ” suspension ” of your file until the issue is resolved.

Fix: Before you even apply, gather your last 2 years of tax returns last 30 days of pay stubs last 2 months of bank statements, and any documentation for additional income sources have it all in a digital folder ready to submit instantly.

2. Complex Financial Profiles

Self employed Multiple income streams Own rental properties Your file will take longer because the underwriter needs to manually verify and calculate income that doesn’t fit a neat W-2 box self-employed borrowers in particular should expect to provide 2 full years of business tax returns a year-to-date profit and loss statement and potentially a CPA letter confirming business viability .

Fix: Work with a loan officer who specializes in self employed borrowers they’ll know exactly what the underwriter needs upfront saving you multiple rounds of back and forth.

3. Low Appraisal

If the appraised value comes in below the purchase price the lender won’t fund the full loan amount this can derail or delay the entire process while you renegotiate with the seller or come up with additional cash .

Fix: Research comparable sales in the area before making an offer if you’re in a hot market build an appraisal gap clause into your contract so you’re prepared .

4. Title Issues

Liens unpaid property taxes boundary disputes or errors in the chain of ownership can surface during the title search and require legal resolution before closing can proceed .

Fix: This one is largely out of your hands but choosing a reputable title company and starting the search early helps ask your lender to order the title search the same day your application is submitted .

5. Mid-Process Financial Changes

Opening a new credit card financing a car making a large cash deposit or changing jobs during underwriting is the equivalent of throwing a wrench into a running engine any of these changes will trigger a re-verification of your entire financial profile .

Fix: Treat the underwriting period like a financial freeze don’t change anything no new credit no big purchases no job changes until you have the keys in your hand .

Automated vs Manual Underwriting : Why It Matters for Your Timeline

Not all underwriting is created equal the method your lender uses has a massive impact on how long you’ll wait .

| Factor | Automated Underwriting (AUS) | Manual Underwriting |

|---|---|---|

| Speed | Minutes to hours for initial decision | Days to weeks |

| Best For | Standard W-2 borrowers, clean credit | Self-employed, thin credit, unique situations |

| Flexibility | Rigid — follows preset guidelines | High — allows case-by-case exceptions |

| Consistency | Highly consistent, no human bias | Subject to individual judgment |

| 2026 Trend | AI-augmented with IDP and NLP | Human-in-the-Loop (HITL) hybrid models |

[UNIQUE INSIGHT] The AI-Augmented Underwriter : 2026’s Game Changer

Here’s what most guides won’t tell you the underwriter reviewing your file in 2026 is likely working alongside AI tools that didn’t exist two years ago. Modern lenders are deploying Intelligent Document Processing ( IDP ) systems that use OCR and Natural Language Processing to read extract and validate data from your bank statements and tax returns automatically. What used to take an underwriter 3–4 hours of manual document review now takes minutes.

But here’s the catch this doesn’t eliminate the human underwriter It amplifies them the AI handles the data extraction “grunt work” freeing the certified mortgage underwriter to focus on the nuanced judgment calls that algorithms still can’t make evaluating compensating factors assessing the ” story ” behind an unusual financial pattern or deciding whether a borderline DTI ratio is actually acceptable given the borrower’s overall profile .

The result? Lenders with modern tech stacks are closing loans 30–60% faster than those still running on legacy systems if speed matters to you ask your lender directly : ” Do you use automated document processing in your underwriting pipeline ? “

Underwriting Timelines by Loan Type

The type of loan you’re applying for also affects how long underwriting takes. Here’s a realistic breakdown

| Loan Type | Typical Underwriting Time | Why |

|---|---|---|

| Conventional | 2–4 weeks | Streamlined AUS process; fastest for clean files |

| FHA | 3–5 weeks | Additional property requirements and MIP calculations |

| VA | 3–6 weeks | VA appraisal process and Certificate of Eligibility verification |

| USDA | 4–6 weeks | Requires two rounds of underwriting (lender + USDA office) |

| Jumbo | 3–6 weeks | Higher scrutiny on income/assets due to larger loan amounts |

| Refinance | 2–5 weeks | No purchase agreement, but appraisal and existing loan payoff add steps |

How to Speed Up Your Underwriting : A Practical Checklist

You’ve seen the delays now here’s how to beat them follow this checklist and you’ll put yourself in the fastest lane possible :

- Pre organize Your Documents : Before applying compile tax returns (2 years) pay stubs (30 days) bank statements (2 months) and government issued ID in a single digital folder .

- Disclose Everything Upfront : Past bankruptcies judgments or gaps in employment ? Tell your loan officer on Day 1 Surprises during underwriting cause the worst delays .

- Respond to Conditions Within 24 Hours : When the underwriter asks for something, drop everything and provide it every day you delay adds a day (or more) to your closing .

- Freeze Your Finances : No new credit applications no large purchases no job changes and no large unexplained deposits until after closing .

- Choose Your Lender Wisely : Ask about their current pipeline volume and average closing time a lender with a 30 day average will serve you better than one averaging 55 days .

- Ask About Technology : Lenders using desktop underwriting platforms and AI document processing close faster it’s a legitimate question to ask before committing .

What Happens If You Get Denied During Underwriting ?

Let’s address the elephant in the room not every underwriting story ends with a ” Clear to Close ” Denial happens and it’s more common than you might think .

The most frequent reasons for underwriting denial include :

- DTI ratio too high : Most lenders cap DTI at 43 50% If your debts consume too much of your income you won’t qualify .

- Credit score drop: If your score falls below the minimum threshold during the process (often due to a new credit inquiry or late payment) the loan can be denied .

- Employment change: Switching jobs especially from salaried to commission based during underwriting is a red flag that can result in denial .

- Appraisal shortfall: If the property doesn’t appraise at the purchase price and you can’t bridge the gap the loan falls through.

- Undisclosed debt: If the underwriter discovers liabilities you didn’t report it damages your credibility and can result in immediate denial.

If you’re denied your lender is legally required to send you an Adverse Action Notice explaining the specific reasons Use that information to fix the issues before reapplying. In many cases, a denial today can become an approval in 3–6 months with targeted credit repair and debt reduction .

The Outsourcing Factor : Why Lender Efficiency Varies So Much

Here’s something borrowers rarely consider : the speed of your underwriting depends heavily on how your lender has structured its operations behind the scenes

Many mid sized lenders and brokers in the US now outsource portions of their underwriting workflow to specialized firms that handle document processing income verification and preliminary file review this isn’t a shortcut it’s a strategic move By leveraging dedicated home loan underwriting teams that operate across time zones lenders can process files around the clock instead of being limited to a single shift .

The result A file that might sit untouched for 3 days at an overloaded in house operation gets reviewed within hours by a specialized team If you’re comparing lenders, ask about their operational model the ones who’ve invested in efficient underwriting operations will consistently deliver faster timelines without cutting corners on quality

Frequently Asked Questions

How long does mortgage underwriting take on average?

Mortgage underwriting typically takes between 1 and 6 weeks. The overall time from application to closing averages 42–45 days, with underwriting being the most variable phase. Straightforward files with clean W-2 income can clear in under two weeks, while complex self-employed files may take the full six weeks.

Can underwriting be done in one day?

The automated portion can. Systems like Fannie Mae’s Desktop Underwriter return a preliminary decision in minutes. However, full underwriting—including document verification, appraisal review, and condition clearing—still requires several days at minimum, even with the most efficient lenders.

What causes delays during the underwriting process?

The most common causes are missing documentation, complex income verification (self-employment), low property appraisals, title issues, and borrowers making financial changes mid-process. Responding promptly to underwriter requests is the single most effective way to prevent delays.

What is the difference between automated and manual underwriting?

Automated underwriting uses algorithms to assess risk in minutes, ideal for standard borrowers with clean files. Manual underwriting involves a human reviewer who evaluates each document individually, taking days to weeks but offering flexibility for borrowers with unique financial situations, thin credit, or compensating factors that algorithms can’t properly weigh.

How can I speed up the underwriting process?

Provide complete documentation upfront, respond to all conditions within 24 hours, avoid any financial changes during the process, and choose a lender with modern technology and manageable pipeline volume. Borrowers who are proactive and responsive consistently close faster than those who aren’t.

Need Underwriting That Doesn’t Slow You Down?

Whether you’re a lender looking to scale or a borrower trying to understand the process, having the right underwriting team makes all the difference. Capstone Planet provides specialized mortgage underwriting support that helps US lenders close faster, with zero compromises on accuracy.

{kind=link}

{kind=link}

{kind=link}