What is a Mortgage Underwriter in 2026?

A mortgage underwriter is a financial risk expert who determines a borrower’s eligibility for a home loan by auditing their credit, capacity and collateral. In 2026 the role has evolved into a hybrid intelligence position where human underwriters use AI driven systems to verify financial data in real time. The underwriter is the final decision maker who issues the “Clear to Close” or loan denial based on federal compliance and lender risk standards.

What is a Mortgage Underwriter? (The Gatekeeper of Risk)

In the 2026 lending landscape the mortgage underwriter acts as the ultimate “detective” while loan officers and processors gather documents the underwriter synthesizes the risk. They ensure that every loan funded by the bank is a safe long term investment that complies with updated 2026 federal regulations.

Underwriters at leading firms like CapStonePlanet now leverage machine learning to automate 85% of data verification. This allows the human professional to focus on high level risk logic and complex files that involve non traditional income or unique property types. If you’re curious about how this compares to other industries consider the insurance underwriter which manages similar risk structures but for policy premiums rather than mortgage backed assets.

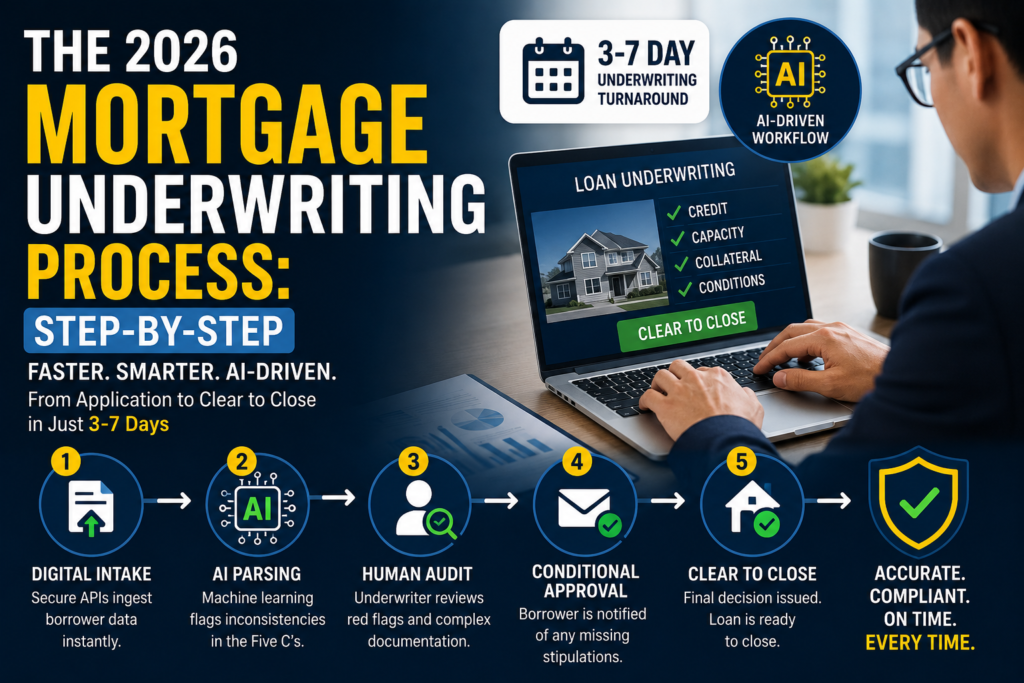

Step by step infographic explaining the AI powered mortgage underwriting process from application review to final clear to close approval.

The 2026 Mortgage Underwriting Process: Step-by-Step

Efficiency is the benchmark of 2026. The mortgage underwriting process has been compressed into a 3-7 business day window for standard files.

- Digital Intake: Secure APIs ingest employment and asset data instantly.

- AI Parsing: Machine learning flags any inconsistencies in the “Five C’s” (Credit, Capacity, Capital, Collateral and Conditions).

- Human Audit: A senior underwriter reviews “red flags” and complex documentation.

- Conditional Approval: The borrower is notified of any missing “stipulations.”

- Clear to Close: The final “gold standard” decision is issued.

For a more granular look at the timeline visit our Step-by-Step Process Guide.

Common Reasons for Underwriting Denial (and How to Avoid Them)

Even with high tech tools loans are still denied. Understanding these common “fatal flaws” can save your closing:

- Unverifiable Deposits: Large cash deposits without a clear paper trail (gift letters are mandatory in 2026).

- Employment Gaps: AI systems flag sudden job changes within 60 days of closing.

- New Debt: Financing a car or opening new credit cards during the underwriting window.

- Appraisal Gaps: When the property value comes in lower than the purchase price.

Strategy: Always keep your finances “frozen” from the moment you apply until you receive your keys.

Mortgage Underwriter Salary & Industry Outlook 2026

The mortgage underwriter salary in 2026 is at an all time high due to the technical complexity of the role lenders are paying a premium for underwriters who can manage AI driven workflows.

| Role Tier | 2026 Salary Range |

|---|---|

| Junior/Associate Underwriter | $75,000 – $92,000 |

| Senior Underwriter (DE/SAR) | $118,000 – $148,000+ |

Explore the full state by state breakdown here: Mortgage Underwriter Salary Guide.

How to Become a Mortgage Underwriter in 2026

Success in this field requires a blend of financial literacy and technical proficiency. Most professionals start as Loan Processors often working with BPO companies to learn the documentation side of the business.

The 2026 Elite Path:

- Earn a Bachelor’s in Finance or Economics.

- Gain 2 years of experience in loan processing.

- Master Automated Underwriting Systems (AUS).

- Obtain FHA Direct Endorsement (DE) authority.

See the full roadmap: How to Become a Mortgage Underwriter in 2026.

Frequently Asked Questions

What does a mortgage underwriter do?

A mortgage underwriter evaluates a borrower’s financial risk by auditing their credit history income stability assets and the property’s appraised value. Their goal is to ensure the loan meets all lender and federal guidelines before issuing a final approval.

What is the salary of a mortgage underwriter in India?

In 2026 a mortgage underwriter in India typically earns between ₹4,50,000 to ₹12,00,000 per annum. Salaries vary based on experience and whether the underwriter specializes in domestic or international (e.g., US/UK) mortgage markets.

What are the 4 C’s of mortgage underwriting?

The 4 C’s are Credit (repayment history) Capacity (ability to pay/DTI), Capital (assets and reserves) and Collateral (property value). Many elite 2026 lenders also add a 5th C: Conditions.

What is the difference between a loan officer and an underwriter?

A loan officer is your primary point of contact who helps you select a loan and collects your paperwork. The underwriter works behind the scenes to verify that paperwork and make the final “Yes” or “No” decision on the loan approval.

Is mortgage underwriting a stressful job?

It can be fast paced, especially during high volume periods. However 2026’s AI tools have significantly reduced the “grunt work,” allowing underwriters to focus on creative problem solving.

What is a “Clear to Close” in mortgage underwriting?

This is the final approval. It means the underwriter has reviewed all conditions and the loan is ready for funding. Once you hear “Clear to Close” your keys are just days away.

Editorial Accuracy & Trust

This master guide is authored by Shubham Pathak, a leading voice in mortgage operations and AI driven finance. Each section is reviewed by CapStonePlanet’s internal compliance team to ensure factual accuracy and alignment with 2026 lending standards.

{kind=link}

{kind=link}