What is Mortgage Underwriting in 2026?

At its core underwriting is the process where a lender verifies your income, assets, debt and property details to decide if they should back your loan. In 2026 this “risk analysis” is increasingly performed by Automated Underwriting Systems (AUS) that use machine learning to predict repayment probability with higher accuracy than legacy manual methods.

Factual Backing: Modern underwriting models now include “Alternative Credit Data,” such as on time rent and utility payments which has expanded mortgage access to an estimated 15% more borrowers globally compared to five years ago. To understand the foundational role of an underwriter you can explore our detailed guide on what is an underwriter in 2026.

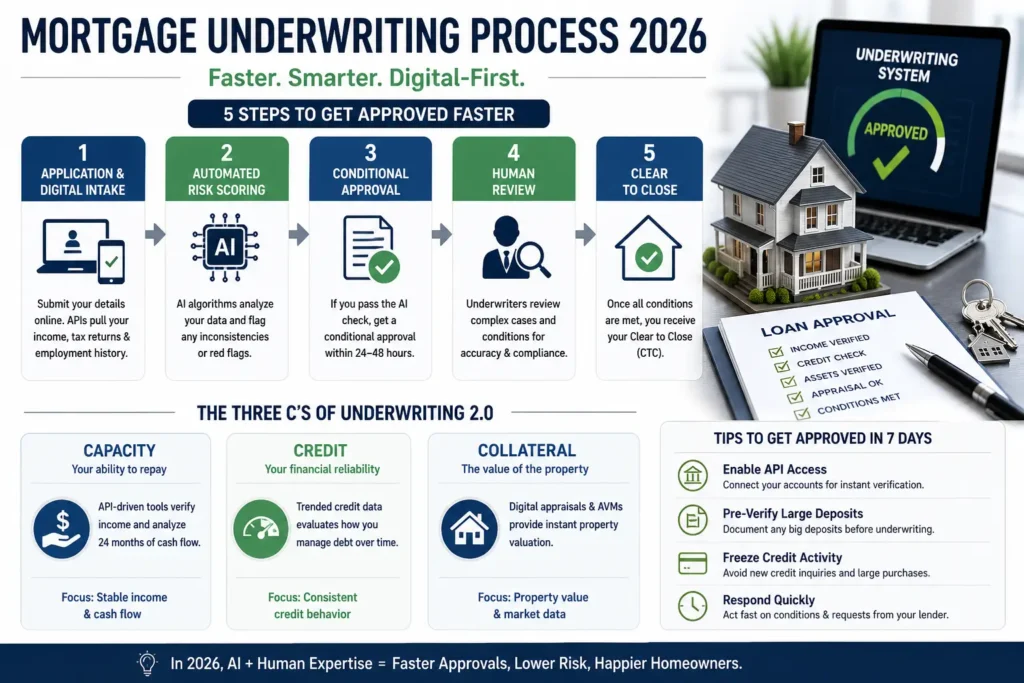

Step-by-step mortgage underwriting process in 2026 including the 5 approval stages and the three Cs of underwriting.

The Three C’s of Underwriting 2.0

While the fundamentals remain the same, the way lenders verify them has changed:

- Capacity: Your ability to repay lenders now use API driven tools like Plaid to pull 24 months of verified cash flow directly from your bank often replacing the need for physical paystubs.

- Credit: Your financial reliability beyond just a FICO score 2026 underwriting looks at ” Trended Credit Data ” how you manage debt over time rather than just a snapshot in time.

- Collateral: The value of the property digital appraisals and Automated Valuation Models (AVMs) are now standard allowing for instant property verification in many urban markets.

The 5 Steps of the 2026 Underwriting Process

- Application & Digital Intake: You submit your data via a secure portal APIs automatically pull your tax returns and employment history.

- Automated Risk Scoring: The system runs your data through an AI model to flag any inconsistencies or “red flags” immediately.

- Conditional Approval: If you pass the AI check you receive a conditional approval often within 24–48 hours.

- The Human Review: A professional mortgage underwriter reviews the “complex” parts of your file that AI might flag. Many leading firms now utilize third-party service providers to handle this volume while maintaining strict compliance.

- Clear to Close: Once all conditions (like the appraisal or proof of insurance) are met you receive the “Clear to Close” (CTC).

How to Get a 7-Day Approval

To move through the mortgage underwriting process faster follow these 2026 best practices:

| Action | Why it Matters |

|---|---|

| Enable API Access | Allowing your lender to link directly to your accounts (Plaid/Encompass) eliminates manual document review time. |

| Pre-Verify Large Deposits | Document any non payroll deposits over $500 before the underwriter even asks. |

| Freeze Credit Activity | Do not open new credit cards or make large purchases during the “active” underwriting phase. |

If you encounter delays it may be helpful to consult with a professional outsourcing service provider who understands the intricacies of digital loan processing.

Frequently Asked Questions (FAQ)

How long does mortgage underwriting take in 2026?

With the integration of AI driven digital verification the average mortgage underwriting process now takes between 5 to 10 business days. However high efficiency lenders utilizing 100% digital workflows can provide conditional approvals in as little as 24–48 hours.

What is the most common reason for a mortgage underwriting denial?

In 2026 the most common reasons remain Debt-to-Income (DTI) ratio issues and “undisclosed debt.” Even with AI scoring large recent purchases or new credit lines during the active phase can trigger an automatic denial.

Do I need to submit physical paystubs in 2026?

Generally no. Most modern lenders use API based verification (like Plaid) to verify income directly from your bank or employer. Physical paystubs are now typically only required for complex self employment cases or non traditional income streams.

Can I speed up the underwriting process?

Yes. By enabling instant digital verification and providing “letters of explanation” for large deposits upfront you can significantly reduce manual review time and move to “Clear to Close” faster.

About CapStonePlanet

CapStonePlanet is a leading professional services firm providing specialized BPO, mortgage underwriting and digital consulting services to US based firms. As a contributor to the company’s knowledge base this article was developed after thorough research and collaboration with CapStonePlanet’s internal underwriting experts. Our mission is to scale business operations through technical excellence and streamlined digital workflows.

{kind=link}

{kind=link}