Quick Answer: What Is Manual Underwriting?

Manual underwriting is when a human mortgage underwriter personally reviews your full financial file instead of relying on an automated system. It is used when borrowers have no credit score, past credit events (like bankruptcy), high debt or unique income situations that algorithms cannot fairly evaluate. In 2026 FHA, VA, and USDA loan programs all still support manual underwriting for qualified borrowers.

What Is Manual Underwriting on a Mortgage?

Manual underwriting is a mortgage approval process where a licensed human underwriter reviews your application file from scratch your income documents, bank statements, employment history and payment records without relying solely on an automated credit score.

It is the opposite of automated underwriting (AUS) which uses algorithms to issue instant approvals.

Manual underwriting is typically triggered when:

- Your file receives a “Refer” or “Caution” finding from the AUS

- You have no FICO credit score (a “thin file”)

- You had a bankruptcy, foreclosure or short sale within the past 1-4 years

- Your Debt to Income (DTI) ratio exceeds standard automated limits

- Your income comes from self employment, rental properties or non traditional sources

Manual underwriting is not a punishment. It is simply a different path to the same destination a mortgage approval.

Manual Underwriting vs Automated Underwriting: Key Differences

| Feature | Automated (AUS) | Manual Underwriting |

|---|---|---|

| Reviewer | Algorithm / Software | Licensed Human Underwriter |

| Speed | Minutes to hours | 1–4 weeks |

| Credit Score Required? | Usually yes (620+) | No (can use alternative credit) |

| Documentation | Standard | Extensive (12–24 months) |

| Flexibility | Low | High (compensating factors matter) |

| Best For | Standard borrowers | Complex or unique financial profiles |

| Loan Types | Conventional, FHA, VA, USDA | FHA, VA, USDA (not typically conventional) |

Who Qualifies for a Manually Underwritten Loan?

Manual underwriting is not available for every loan type. In 2026 it is primarily used for government backed loans: FHA, VA and USDA. Conventional loans (Fannie Mae / Freddie Mac) very rarely allow manual review.

The “No Credit Score” Borrower

You have never had a credit card, auto loan or installment debt. The major credit bureaus have no file on you. Your FICO score is listed as “0” or “N/A.” This is common among:

- People who live debt free by choice (Dave Ramsey followers)

- Recent immigrants

- Young adults entering the housing market for the first time

For these borrowers the underwriter builds what is called an “alternative credit history” using 12 months of on time payments for:

- Rent (verified by landlord letter or canceled checks)

- Utility bills (electric, gas, water)

- Phone bills (cell or landline)

- Insurance premiums (auto, renters or life)

The Post Credit Event Borrower

You had a financial hardship a bankruptcy foreclosure or short sale but have since rebuilt your finances manual underwriting allows lenders to look beyond the event and evaluate your current stability.

Waiting period guidelines (2026):

- FHA after Chapter 7 Bankruptcy: 2 years

- FHA after Foreclosure: 3 years

- VA after Bankruptcy: 2 years

- USDA after Foreclosure: 3 years

The High DTI Borrower

Your Debt to Income ratio is above the automated threshold but you have strong compensating factors that an algorithm cannot weigh. This is where a human underwriter’s judgment becomes critical.

FHA, VA and USDA Manual Underwriting Guidelines (2026)

FHA Manual Underwriting DTI Limits

FHA is the most common path for manual underwriting. Here are the 2026 DTI rules:

| DTI Scenario | Front-End Ratio | Back-End Ratio |

|---|---|---|

| Standard (no compensating factors) | 31% | 43% |

| With 1 compensating factor | 37% | 47% |

| With 2+ compensating factors | 40% | 50% |

Common FHA Compensating Factors:

- Verified cash reserves of at least 3 months of mortgage payments

- Minimal payment shock (new payment is less than 5% higher than current rent)

- Stable employment for 2+ years with the same employer

- Additional income not counted in qualifying (overtime, part time work)

- Residual income exceeding VA guidelines for your region

VA Manual Underwriting (For Veterans)

VA loans are uniquely flexible. The VA does not enforce a hard DTI cap for manually underwritten loans. Instead, the underwriter focuses on residual income the money left over after paying all debts, taxes and housing costs each month.

| Family Size | Northeast | Midwest | South | West |

|---|---|---|---|---|

| 1 | $450 | $441 | $441 | $491 |

| 2 | $755 | $738 | $738 | $823 |

| 3 | $909 | $889 | $889 | $990 |

| 4 | $1,025 | $1,003 | $1,003 | $1,117 |

| 5 | $1,062 | $1,039 | $1,039 | $1,158 |

Regional minimum monthly residual income (VA guidelines, 2026). Amounts in USD.

A veteran with a DTI above 41% can still get approved if their residual income exceeds the table minimum by 20% or more.

USDA Manual Underwriting

USDA manual underwriting is triggered when a file doesn’t receive an “Accept” result through the Guaranteed Underwriting System (GUS).

| Scenario | Front-End | Back-End |

|---|---|---|

| Standard | 29% | 41% |

| With compensating factors | 32–34% | Up to 44% |

What Are “Compensating Factors” and Why Do They Matter?

A compensating factor is a financial strength that offsets a perceived risk. When your DTI is high or your credit history is thin, compensating factors are what tip the scales in your favor. Think of them as your “points” with the underwriter.

| Compensating Factor | Why It Helps |

|---|---|

| Large cash reserves (3–12+ months) | Proves you can handle payment if income dips |

| Low payment shock (< 5%) | Shows you’re not overextending vs. current rent |

| Long-term stable employment (2+ years) | Reduces income risk |

| Significant down payment (10–20%+) | Reduces lender’s collateral risk |

| Additional non-qualifying income | Shows financial depth |

| History of managing similar debt levels | Proves behavioral creditworthiness |

The more compensating factors you can document, the higher DTI the underwriter can approve.

What Documents Does Manual Underwriting Require?

Expect to provide significantly more paperwork than a standard mortgage here is the 2026 document checklist:

- ✅ 24 months of tax returns (personal and business if self employed)

- ✅ 12–24 months of bank statements (all accounts, all pages)

- ✅ 12 months of alternative credit history (rent ledger, utility statements)

- ✅ Letter of Explanation (LOE) for any credit events, employment gaps or large deposits

- ✅ Written Verification of Employment (VOE) from employer

- ✅ Gift letters if any portion of the down payment is a gift

- ✅ 12 months of canceled checks or landlord letter (for rental history)

Pro tip: Have these documents organized before you apply. A disorganized file slows the process and signals to the underwriter that you may be hiding something. Organized borrowers get faster approvals.

How Long Does Manual Underwriting Take?

Manual underwriting is slower than automated approval here is a realistic 2026 timeline:

| Stage | Automated Underwriting | Manual Underwriting |

|---|---|---|

| Initial Review | Hours | 3–5 business days |

| Document Collection | 1–3 days | 5–10 business days |

| Final Decision | 24–48 hours | 7–14 business days |

| Total (Estimate) | 5–10 days | 3–6 weeks |

The timeline depends heavily on how quickly you respond to document requests. In manual underwriting, your speed is the underwriter’s speed.

Many borrowers turn to credit unions and FHA-approved lenders for manual underwriting mortgage approvals in 2026.

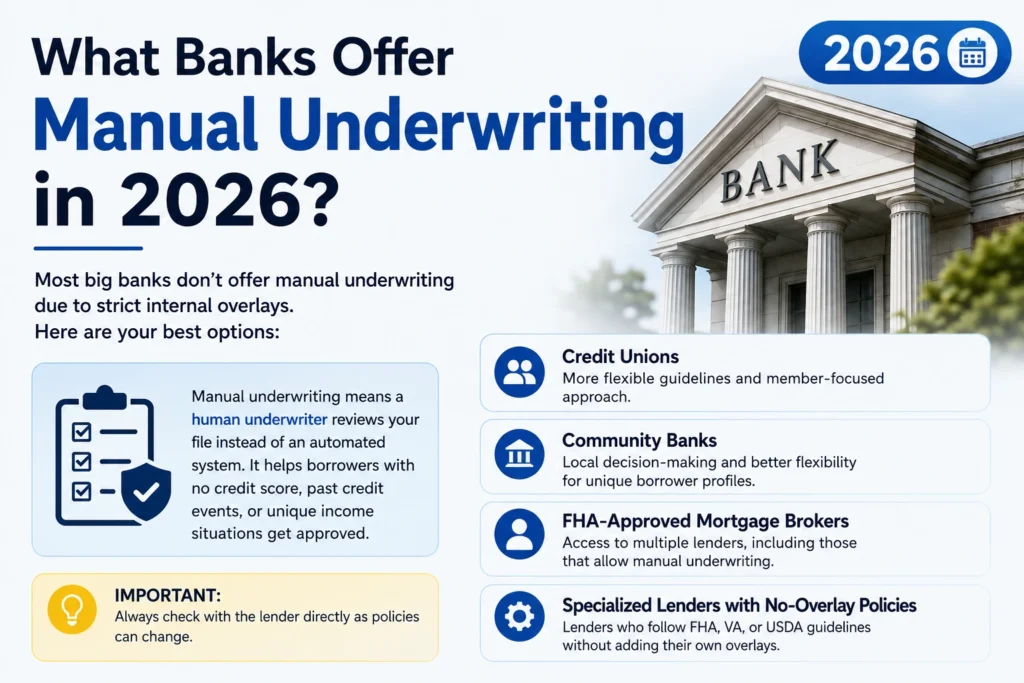

What Banks Offer Manual Underwriting in 2026?

This is the most important question and the answer is: not all of them.

Large banks (Chase, Wells Fargo, Bank of America) often have strict “lender overlays” their own internal rules stricter than FHA/VA/USDA guidelines. Many will not manually underwrite loans at all.

Where to look for manual underwriting lenders:

- Credit Unions: Often more flexible and willing to review complex files

- Community Banks: Local institutions that understand local income patterns

- FHA-Approved Mortgage Brokers: Work with dozens of lenders to find one willing to manually underwrite your file

- Non-QM Lenders: Specialize in loans that fall outside typical automated systems

- Specialized Lenders: Companies known for no overlay manual underwriting policies

Important: Always ask the lender directly: “Do you have overlays on manual underwriting?” A lender with no overlays follows only the official FHA/VA/USDA guidelines giving you the best approval odds.

Does Manual Underwriting Affect Your Interest Rate?

The honest answer: sometimes slightly. Manual underwriting does not automatically mean a higher rate. However because manually underwritten loans carry more perceived risk some lenders may price them 0.125% to 0.25% higher than a standard automated approval.

Shopping at least 3 lenders is essential to avoid overpaying.

How Manual Underwriting Fits Into the Full Mortgage Process

Manual underwriting is one step inside the larger mortgage approval journey here is where it fits:

- Pre-qualification → You estimate your budget

- Pre-approval → Lender reviews initial documents

- Loan Submission → Your file is submitted to underwriting (learn what happens here)

- AUS Decision → Software reviews your file

- Manual Review (if triggered) → Human underwriter takes over ← You are here

- Conditional Approval → Underwriter requests additional documents

- Clear to Close → All conditions met approval is final

If you’re worried about what any stage of this process means for your approval odds our full guide Should I Be Worried About Underwriting? — walks you through every outcome in plain language.

Tips to Maximize Your Manual Underwriting Approval Odds

- Build your alternative credit file before applying. 12 months of documented on-time rent and utility payments significantly strengthens a no score application.

- Pay down debt aggressively. Every percentage point you drop your DTI below 43% improves your file.

- Avoid new credit applications during the process. New inquiries can flag the underwriter.

- Write a clear, honest Letter of Explanation. If you had a bankruptcy or a gap in employment a clear, factual explanation builds trust.

- Choose the right lender. Do not waste time with banks that have overlays. Work with an FHA approved broker or a no overlay lender from the start.

- Have your documents organized. Present your file like a business plan. Tabs, labels and a cover letter make a difference.

Frequently Asked Questions

What is manual underwriting for a mortgage?

Manual underwriting is one part of the larger mortgage approval system handled by professional underwriters. For a deeper breakdown of underwriting careers salary structures and loan review workflows read our Mortgage Underwriter Master Guide.

What banks offer manual underwriting?

Most big banks do not actively offer manual underwriting due to internal overlays. Your best options are credit unions, community banks, FHA approved mortgage brokers and specialized lenders with no overlay policies. Always ask: “Do you have overlays on FHA manual underwriting?”

Can I get a mortgage with no credit score through manual underwriting?

Yes FHA and VA loans allow manual underwriting for borrowers with no FICO score. The underwriter uses 12 months of alternative payment history rent, utilities, phone bills to establish your creditworthiness.

Does manual underwriting take longer?

Yes. Manual underwriting typically takes 3 to 6 weeks total, compared to 5–10 days for automated approvals. You can speed up the process by responding to all document requests immediately and having your paperwork organized in advance.

What DTI do I need for FHA manual underwriting?

With no compensating factors: 31% front-end / 43% back-end. With one strong compensating factor: up to 37% / 47%. With two or more compensating factors: up to 40% / 50%.

Is manual underwriting harder to pass?

It requires more documentation and scrutiny but it is specifically designed to help borrowers who cannot pass automated underwriting. With the right compensating factors and an organized file many borrowers who were rejected by an AUS are successfully approved through manual review.

Bottom Line: Manual Underwriting Is Not a Last Resort It’s the Right Tool

If you’ve been told you “don’t fit the system” manual underwriting exists precisely for you. It takes longer and requires more paperwork. But for millions of borrowers veterans, debt free families self employed professionals and recent bankruptcy survivors it is the only path to homeownership.

The key is finding a lender who has experience with manual files and walking in with an organized, honest, well documented application.

{kind=link}

{kind=link}

{kind=link}