Reviewed by Shubham Pathak, Senior Underwriting Consultant | Updated May 11, 2026

Should I be worried about underwriting? No. It is a standard verification phase, not an interrogation. As long as your finances are stable and you have been honest on your application you are on a predictable path to underwriting approval. In 2026 over 90% of vetted applications move successfully from submission to Clear to Close.

If you are reading this while staring at a silent phone or a portal that says “Under Review” take a deep breath You are doing great. That knot in your stomach is normal but it doesn’t mean your loan underwriting is in trouble. Before this stage, you likely received a pre approval, but underwriting is simply the lender double checking the math so you can walk into your new home with total confidence.

The Calm Reality: What is Underwriting?

What is underwriting? At its core it is the final safety check where a lender verifies that your financial reality matches your application. The underwriting process is not a trap; it is a partnership. The lender wants to give you this loan they just need to prove to the federal regulators that they did their homework. Many borrowers ask, “what does underwriting mean?” specifically in the 2026 market. It means that a human mortgage loan underwriter, supported by AI auditing tools is confirming you can afford the home long term.

🛑 What NOT To Do During Underwriting (The Golden Rules)

To keep your mortgage loan underwriting process on the fast track you must keep your financial life “boring” and static. The underwriter is reviewing a “snapshot” of your life if that snapshot changes the review has to start all over again. Follow these rules strictly:

- Don’t open new credit cards: This can disrupt the credit underwriting process.

- Don’t finance furniture: Wait until the keys are in your hand to buy that sofa.

- Don’t buy or lease a car: This is the #1 cause of last-minute loan denials.

- Don’t change jobs: Stability is the key for income verification during a home loan underwriting review.

- Don’t move large sums of money: Keep your bank accounts steady for audit trails.

Real World Case Study: From Panic to Keys

Sarah’s Story: The Missing Page

The Panic: Sarah received a notice to submit to underwriting a missing page of a bank statement from 2024. She panicked, thinking the bank was suspicious of her savings.

The Reality: It was simply a compliance check. The underwriter noticed Page 6 of 7 was missing from a PDF upload. The AI system flagged it as “incomplete data.”

The Outcome: Sarah uploaded the page that afternoon. The underwriter cleared the condition in 4 hours, and Sarah received her underwritten approval the next morning.

How Long Does Underwriting Take? (2026 Stats)

A common concern is how long does underwriting take for a home loan. According to hard data from the Mortgage Bankers Association (MBA) the vast majority of borrowers who reach the underwriting stage finish the process successfully and on time. For military families, the VA loan underwriting timeline follows a slightly different set of benchmarks.

| Metric | Conventional Loans | FHA Loans |

|---|---|---|

| Average Mortgage Underwriting Process Time | 4-6 Days | 6-9 Days |

| Overall Approval Rate | 91.2% | 88.5% |

*If you’re wondering how long for underwriting after a credit pull, most initial reviews start within 48 hours.

Underwriting Approval vs. Clear to Close

Many borrowers get confused when they hear “you’re approved,” but then receive a long list of tasks. Here is the breakdown of the loan underwriting process milestones:

Conditional Approval

This is the “Green Light with a To-Do List.” It is a massive win and means 90% of the underwriting for a mortgage loan is done.

Clear to Close (CTC)

This is the finish line. The underwriter has cleared every condition and the audit is finished.

What Happens During Underwriting?

Knowing exactly what happens during underwriting can help manage your expectations regarding wait times. This phase involves both high-speed AI scans and detailed human audits. This is a deeper look at the technical mortgage underwriting process that every file undergoes. One critical step is the underwriting before appraisal check where the lender verifies your income and assets before spending money on the property inspection. For those wondering how long does the underwriting process take for a mortgage, the answer usually depends on how fast you can provide requested documents.

The Complete Mortgage Documents Checklist

Stay ahead of the curve by preparing a robust mortgage documents checklist. By having your W-2s and tax returns ready, you reduce the chances of delays in your underwriting process for home loan. Check out our production-ready mortgage papers checklist to see exactly what you need.

How Underwriters Review Your Tax Returns

If you are self employed, the underwriter will analyze your IRS filings for consistency. This is a standard part of the credit underwriting process for non traditional earners. Learn more in our guide to how underwriters review tax returns. They are looking for your “Net Income” to ensure you have the capacity to comfortably afford the new monthly payment.

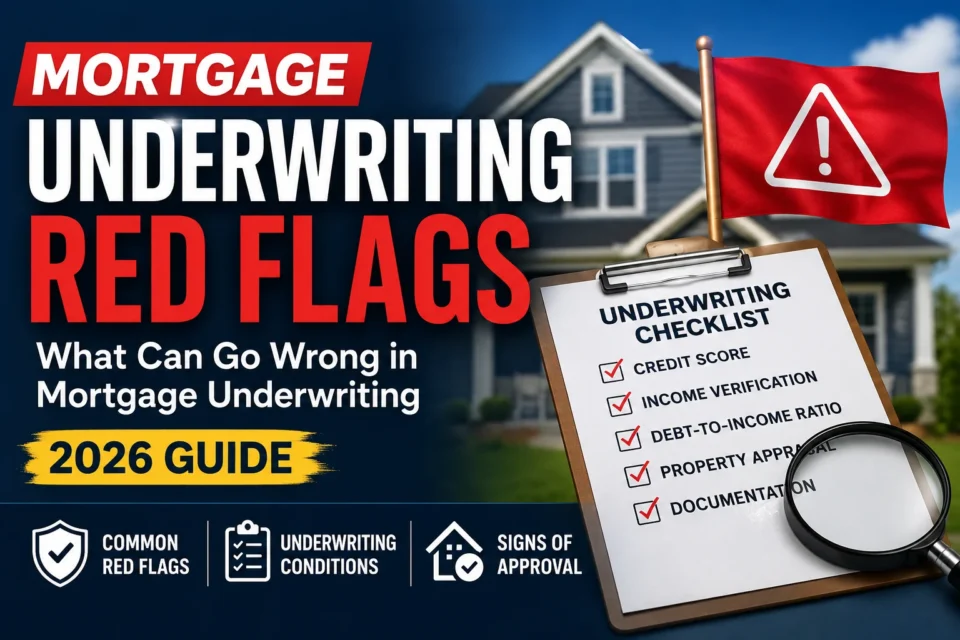

Mortgage Underwriting Red Flags to Avoid

By identifying common underwriting red flags early, you can take steps to fix them before they jeopardize your loan. These triggers often include large unexplained deposits or undisclosed debts. We have mapped out the most common pitfalls in our guide to mortgage underwriting red flags and conditions.

Frequently Asked Questions

What is home loan underwriting?

It is the process of a lender verifying your income, assets, credit and the property’s value to ensure the loan meets safety guidelines.

How long does the underwriting process take?

Typically how long does mortgage underwriting take depends on complexity but the industry average in 2026 is 5 to 8 business days. Manual underwriting or complex files may extend this to 10-14 days depending on lender volume.

What does underwriting a loan mean for me?

It means your application is being finalized. What does an underwriter look for specifically? They look for consistency between your words (the application) and your proof (bank statements and pay stubs).

How long does loan underwriting take for a personal loan?

A personal loan underwriting process is much faster than a mortgage, often taking only 24 to 48 hours since there is no property collateral to verify.

How long does underwriting take after conditional approval?

Once you provide your conditions, it usually takes 24 to 48 hours for an underwriter to review the new documents and issue a final approval.

{kind=link}

{kind=link}

{kind=link}