What does a pre approval letter look like?

A mortgage pre approval letter is a one page document printed on official lender letterhead. It states the borrower’s name the maximum approved loan amount the loan program (Conventional, FHA or VA) any conditions of approval and an expiration date usually 60 to 90 days from the date of issue.

1. What Is a Mortgage Pre Approval Letter ?

A loan approval letter is a formal document issued by a licensed mortgage underwriter or lender after they have reviewed your income, assets, credit history and debt to income ratio. It tells sellers and real estate agents that you are a financially verified buyer not just someone browsing listings online. Unlike a pre qualification letter which is based on self reported information a pre approval requires you to submit actual mortgage papers like W-2 forms, pay stubs and bank statements. The lender also performs a hard credit inquiry to verify your FICO score.

Why it matters: In a competitive market sellers frequently reject offers that do not include a pre approval letter because it signals the buyer may not be able to secure financing.

2. Mortgage Pre Approval Letter Template (Full Sample)

Below is a realistic mortgage pre approval letter template based on the standard format used by major lenders across the United States. Your actual letter will be customized by your loan officer.

[LENDER NAME — OFFICIAL LETTERHEAD]

[Lender Address]

[City, State, ZIP Code]

[Phone Number] | [NMLS #]

Date: May 8, 2026

To Whom It May Concern,

This letter confirms that [Borrower Full Name] has been pre-approved for a mortgage loan by

[Lender Name]. This pre-approval is based on a verified review of the borrower’s income, assets,

employment history, and credit profile.

Pre-Approval Details:

- Borrower(s): [Full Legal Name(s)]

- Loan Program: [Conventional / FHA / VA / USDA]

- Maximum Loan Amount: $[Amount]

- Loan Term: [30-Year Fixed / 15-Year Fixed / ARM]

- Interest Rate: Subject to market conditions. This letter does not constitute a rate lock.

Conditions of This Pre-Approval:

- Satisfactory appraisal of the subject property.

- Final review and approval by the underwriting department.

- No material change in the borrower’s financial situation, employment, or credit profile before closing.

- Verification of all submitted documentation.

- Clear title search with no outstanding liens.

Expiration Date: This pre-approval is valid for 90 days from the date of this letter, expiring on

August 6, 2026.

Sincerely,

[Loan Officer Name]

[Title] | NMLS #[Number]

[Lender Name]

Important: You cannot write this letter yourself. It must be issued directly by your licensed lender or mortgage broker after a formal application and credit check.

3. How to Read a Pre Approval Letter Line by Line

Understanding each component of a loan pre approval letter sample helps you spot errors before submitting it with your offer. Here is what every section means:

| Section | What It Means | What to Check |

|---|---|---|

| Lender Letterhead | Proves it came from a licensed institution | Verify the NMLS number is real |

| Borrower Name | Your full legal name as it appears on your ID | Ensure spelling matches your purchase agreement |

| Loan Program | Conventional, FHA, VA or USDA | Confirm this matches the loan type you applied for |

| Maximum Loan Amount | The highest dollar amount you are approved for | You can ask the lender to issue a lower amount to protect your negotiating power |

| Expiration Date | Typically 60–90 days from issue | Never submit an expired letter with your offer |

| Conditions | What must happen before final approval | Appraisal, title search and underwriting review are standard |

Pro tip: Ask your loan officer to issue the letter for a specific amount that matches your offer price not your maximum. Revealing your full buying power to a seller can weaken your negotiation position.

4. Pre Qualification Letter vs Pre Approval Letter : What Is the Difference?

These two terms are frequently confused by first-time homebuyers. While they sound similar, they carry very different weight in the eyes of sellers and real estate agents.

| Feature | Pre Qualification Letter | Pre Approval Letter |

|---|---|---|

| Financial Data | Self reported (unverified) | Verified with documentation |

| Credit Check | Soft pull or none | Hard credit inquiry required |

| Processing Time | Minutes to hours | 1 to 3 business days |

| Seller Confidence | Low — informational only | High — signals serious buyer |

| Loan Guarantee | No | No — but much stronger |

Common mistake: Many buyers assume a pre qualification letter template holds the same value as a pre approval. In multiple offer situations sellers almost always choose the buyer who presents a fully verified pre approval letter.

Documents required for a mortgage pre approval letter including income proof tax returns bank statements and photo ID.

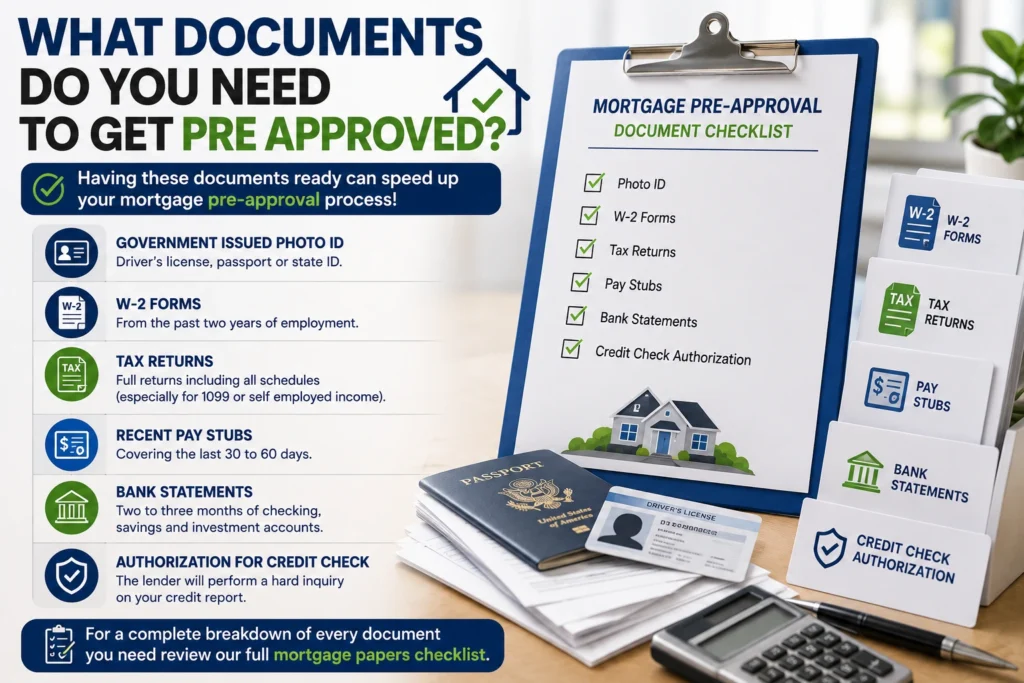

5. What Documents Do You Need to Get Pre Approved?

Before your lender can issue a mortgage pre approval letter template you must submit specific financial documentation having these ready before your initial meeting speeds up the process significantly.

- Government Issued Photo ID: Driver’s license, passport or state ID.

- W-2 Forms: From the past two years of employment.

- Tax Returns: Full returns including all schedules (especially for 1099 or self employed income).

- Recent Pay Stubs: Covering the last 30 to 60 days.

- Bank Statements: Two to three months of checking, savings and investment accounts.

- Authorization for Credit Check: The lender will perform a hard inquiry on your credit report.

For a complete breakdown of every document you need review our full mortgage papers checklist.

6. How Long Is a Pre Approval Letter Valid?

Most lenders issue pre approval letters with a validity period of 60 to 90 days. After this window expires your letter is no longer considered current because your financial situation may have changed.

What happens when it expires? You will need to contact your loan officer resubmit updated pay stubs and bank statements and undergo a new credit check. In most cases, the lender can issue a refreshed letter within a few business days assuming your financial profile has remained stable.

Best practice: If your home search is taking longer than expected contact your lender one to two weeks before the expiration date to begin the renewal process. Do not wait until a seller asks for it.

7. Can You Shop Multiple Lenders Without Hurting Your Credit?

Yes. The credit scoring models used by FICO and VantageScore include a “rate shopping” window. If you apply with multiple mortgage lenders within a 14 to 45 day period all the hard inquiries are grouped together and counted as a single inquiry for scoring purposes.

This means you can and should compare pre approval offers from at least two to three lenders to find the best interest rate and loan terms without worrying about a significant drop in your credit score.

8. Common Mistakes That Weaken Your Pre Approval Letter

Even after you receive your mortgage approval letter, certain actions can invalidate it before you close on a home. Avoid these critical mistakes:

- Changing jobs: Switching employers or going from salaried to self employed disrupts the employment verification that the lender already completed.

- Taking on new debt: Opening a new credit card, financing a car or cosigning a loan changes your debt to income ratio.

- Making large deposits without a paper trail: Unexplained cash deposits in your bank accountwill trigger an underwriting manual review.

- Missing payments: A single late payment on any account during the underwriting period can lower your credit score enough to jeopardize your approval.

- Submitting an expired letter: Always verify the expiration date before attaching your letter to an offer.

It is natural to feel a bit on edge after seeing how easily a pre-approval can be weakened. However, as long as you keep your finances static, you are in a very strong position. If you find yourself asking, “should I be worried about mortgage underwriting?” during this waiting period, remember that most vetted applications move smoothly to the finish line.

9. How Sellers and Real Estate Agents Evaluate Your Letter

In a competitive housing market, your loan approval letter is your first impression with the seller. Here is what experienced listing agents look for when reviewing offers:

- Lender reputation: Local lenders and well known national banks are often preferred over unknown online only lenders.

- Loan type: Conventional loans are generally viewed as the smoothest path to closing. FHA and VA loans, while perfectly valid, sometimes involve additional appraisal requirements.

- Specific vs. generic amounts: A letter tailored to the offer price shows preparedness. A letter showing your maximum capacity may signal a stretch.

- Expiration proximity: A recently issued letter (within 30 days) signals active readiness. A letter nearing expiration raises concerns.

Frequently Asked Questions (FAQ)

What does a pre-approval letter look like?

A mortgage pre approval letter is a one-page document on official lender letterhead. It lists the borrower’s name, the maximum approved loan amount the loan type (Conventional, FHA, VA), the interest rate range, conditions of approval, and an expiration date — typically 60 to 90 days from the issue date.

How long is a mortgage pre approval letter valid?

Most pre approval letters are valid for 60 to 90 days. After expiration, you must resubmit updated financial documents like recent pay stubs and bank statements so the lender can re-verify your creditworthiness.

What is the difference between a pre qualification letter and a pre approval letter?

A pre qualification is a quick, informal estimate based on self reported financial data with no hard credit check. A pre-approval is a formal lender review that requires income documentation, asset verification and a hard credit inquiry making it significantly more credible to sellers.

Can I get a pre approval letter from multiple lenders?

Yes. Shopping multiple lenders within a 14 to 45 day window is encouraged. Credit bureaus treat multiple mortgage inquiries in this timeframe as a single inquiry, so your credit score is minimally affected.

Does a pre approval letter guarantee my mortgage will be approved?

No. A pre approval letter is not a final loan commitment. Final approval depends on a satisfactory property appraisal , title search and a second underwriting review to confirm no changes to your financial situation since the pre approval was issued.

What documents do I need to get a pre approval letter?

You will typically need a government issued ID W-2 forms or tax returns from the past two years recent pay stubs 2 to 3 months of bank statements and permission for a hard credit check.

{kind=link}

{kind=link}